The economic impact of coronavirus hit Rebecca Giles with a one-two punch.

In late March, she and her 5-year-old son got kicked out of a winter rental with a week’s notice, when the owners who were spending the off-season in Florida unexpectedly returned to Maine. Then the customers who used Giles’ cleaning service told her not to come.

Rebecca Giles at her apartment with her son, Andrew Benner. Shawn Patrick Ouellette/Staff Photographer

In an instant, she was living in a $1,180-a-month motel in Winthrop with no income. She depleted her savings to push $500 toward the rent.

Fortunately, a $1,700 federal stimulus check arrived in April. And after first being rejected, Giles finally got $500 from the state’s emergency rental relief program.

By early June, Giles had some of her cleaning customers back. She also found a $650-a-month apartment near Augusta. Giles is finally making money again.

“It was hard the past two months, but I did it,” she said recently. “It was definitely a struggle.”

But the struggle isn’t over. Giles is under pressure to pay her new rent, keep up with car insurance and chip away at the balance on her motel bill through a weekly arrangement with the owner.

In a small way, Giles embodies the plight of many Mainers facing mounting household debt triggered by the coronavirus. Jobs lost. Bills piling up. Government cash and private deferrals providing some stopgap relief.

But as the economy begins to reopen amid a continuing pandemic and a deepening recession, two questions are emerging: Can Mainers pay the bills they accumulated during the crisis? What happens if they can’t?

The answers won’t be known for many months. The economy continues to be propped up by trillions of dollars of government relief money, which is likely to keep flowing this year in some form. At the same time, lenders have deferred payments on mortgages and consumer loans, and many will extend that forbearance at least into the summer.

Those and other measures may delay the day of reckoning. But there’s another variable.

Americans already were burdened at the end of 2019 with a record $14 trillion in household debt, according to the New York Federal Reserve. Mainers had taken on nearly $51 billion in debt by then, according to Experian, the credit rating agency. That’s up 18 percent from the depths of the Great Recession a decade ago.

Not all debt is bad, of course. But workers such as Giles who live paycheck to paycheck can always feel the presence of unaffordable debt, looming nearby. In good times, they’re often able to stay ahead of it.

A booming economy, low interest rates and growing wages created an environment in which the majority of households were spending freely but keeping up with their bills. Experian found in early March that credit scores were remaining strong and loan delinquency rates were at record lows.

That changed virtually overnight. Government-mandated shutdowns to slow the spread of the coronavirus in March and April shuttered businesses and eliminated jobs, leading one in four Americans to file for unemployment insurance this spring. In countless instances, many of the newly unemployed put off paying bills.

That’s what happened to the Brown family in Winthrop.

Nathan Brown is an apprentice with United Association Local 716 of the Maine Plumbers and Pipefitters union. He has been out of work since December, but assignments curtailed because of the pandemic have delayed him from being called back to work. Meanwhile, the bills keep coming, and debt collectors are on the hunt.

“We have people calling whom we owe money to,” said his wife, Ashley Brown. “We have a lot of bills. When I lay them all out on the table, it sort of makes it real.”

Brown said her husband’s $600 weekly unemployment check is critical to buying groceries, paying for car insurance and the cellphone. But the family has no health insurance. And money’s tight enough that they were unable to use their car for a few weeks, because there wasn’t enough money to register it. The couple, who have two young children, also have racked up roughly $5,000 of credit card debt.

The Browns received a $1,200 federal stimulus check, which Ashley Brown said they used for a mortgage payment on their U.S. Department of Agriculture-guaranteed home loan. She said their loan hasn’t qualified for a deferral program.

“The house and the lights,” she said, when asked which bills are a priority. “We try to just sort of keep the place running.”

LATE PAYMENTS ON THE RISE

Housing is a key yardstick for measuring consumer debt. Mortgage and rent payments typically eat up the biggest chunk of the monthly bills consumers pay. Trouble paying for housing is a sign of deeper financial distress among homeowners.

In May, the mortgage data and analytics firm Black Knight reported 3.6 million homeowners nationwide were past due on their payments, the largest number since 2015. But more recently, according to Black Knight, lenders are reporting that late payments on mortgages began falling in early June for the first time since March.

Rebecca Giles watches her son play on a bouncing ball at their apartment. Shawn Patrick Ouellette/Staff Photographer

When the crisis hit, lenders began rolling out deferral programs that let most customers put off paying their mortgages and consumer loans for a few months. Bangor Savings Bank was among them. By early June, 600 customers, making up 3.9 percent of the bank’s residential loan borrowers, had applied for forbearance. That’s only half the national average, and the rate has leveled off since May, according to Jim Donnelly, a vice president at the bank.

To put the rate in perspective, Donnelly said, Bangor Savings has $2 billion of home mortgages on its books. The deferrals involve $71 million, or 4.2 percent of the total.

Donnelly said the bank is planning to extend the program after June, but will scrutinize borrowers more closely to see if they’re still out of work, or perhaps expecting to be called back soon.

Lenders must balance the goal of getting borrowers back on track with the potential that they’ll ultimately be unable to repay their loans and trigger foreclosures. Asked whether he was concerned about past-due accounts accelerating later this year, Donnelly said the bank was anticipating a “next wave” of problem accounts.

“We are planning for and expecting delinquencies to rise,” he said.

Payments more than 30 days overdue are considered delinquent – even those in deferral programs – and banks track these numbers closely. The delinquency rate hit nearly 4.4 percent nationally for the first quarter of the year, but it appears to be much lower in Maine. Donnelly said delinquencies are under 1 percent at Bangor Savings. For context, delinquencies soared nationally to over 10 percent in 2010, in the depths of the previous recession.

An evolving measure of the financial health of Maine’s home loan borrowers is the number asking for continued mortgage relief.

Camden National Bank announced a 90-day loan deferral program in mid-March. By late May, it had 796 deferrals on loans that represented $143 million, or 4 percent of total lending.

This month, Camden National is offering an automatic 90-day extension for customers who say they still need help. But 50 percent of the borrowers currently in the program have told the bank they’re ready to go back to the normal repayment schedule.

That’s a sign that many people have been able to assess their financial situation and feel more confident going forward, according to Renee Smyth, Camden National’s chief experience and marketing officer. Maybe they’ve benefited from a stimulus check, federal relief funds to keep workers on the job, or unemployment insurance.

“If you had asked us a couple of months ago, we wouldn’t have thought that would be the case,” Smyth said.

But whether that confidence can survive the evolving recession is uncertain. The $600 weekly unemployment boost, for instance, is set to end July 31. Camden National is closely watching how well tourism-dependent businesses do this summer. That could be an indicator of whether the bank can expect a second wave of past-due accounts in the months ahead.

“As a bank, where are we next year?” Smyth said. “We are trying to understand, what does this mean for us? We’re certainly worried about some of our customers in the hospitality industry and the people who rely on them.”

HOUSING AT RISK

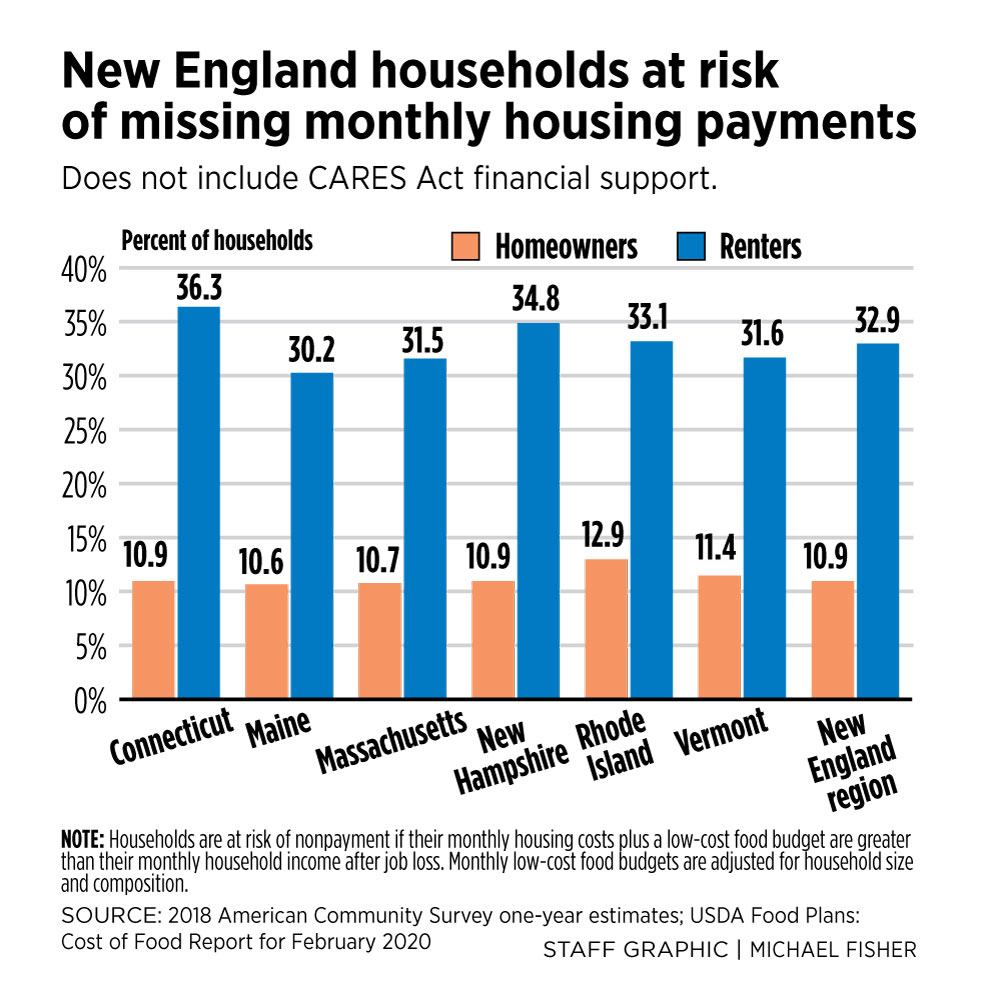

Although Maine has more homeowners than renters, residents who don’t own their homes may be especially vulnerable to the financial disruptions brought on by the pandemic, according to an analysis released in May by the Federal Reserve Bank of Boston.

The bank’s New England Public Policy Center estimated that more than one-third of renters in the six-state region – including 30 percent of renters in Maine — were at risk of not being able to pay their monthly rents. It also found renter households were more likely to be occupied by workers with jobs carrying a higher risk of being shut down during the pandemic. One example is nonessential work that can’t be done remotely, such as Rebecca Giles’ cleaning service.

Renters who can’t pay face the threat of being evicted. Most have a cushion for the moment, because evictions are on hold in Maine until at least Aug. 3, as part of the court system’s COVID-19 phased management plan.

A housing survey done weekly by the U.S. Census Bureau points to signs of future trouble. Nationally, one in five renters weren’t able to pay June rent. In Maine, the figure was better, close to 9 percent. But in another question about confidence in being able to pay next month’s rent, roughly 14 percent of Maine renters indicated they either had no confidence or only slight confidence in being able to do so.

In April, the state also launched a $5 million emergency rent relief program that allocates $500 to eligible households. As of early June, 5,925 applications had been approved for $2.9 million, with about 5,000 applying within the program’s first two weeks. Another 2,779 applications were in the pipeline.

But a one-time $500 contribution won’t go far in places such as Portland, where the average rent is more than $1,400 a month. So housing advocates fear a delayed wave of evictions, once emergency relief money dries up and the court system reopens.

“That is our concern,” said Craig Saddlemire, manager at the Raise-Op Housing Cooperative in Lewiston.

Saddlemire noted that landlords receiving the $500 can’t evict a tenant for nonpayment during that month. But that moratorium won’t carry over into the future, or restrict a landlord from pursuing the balance of the rent due.

“A lot of folks were facing a significant housing crunch before this,” he said. “Now we’re providing some stopgaps for the most vulnerable. But for a real recovery, we need real housing solutions, not homelessness.”

A TALE OF TWO CONSUMERS

As the second half of 2020 comes into focus, uncertainly over the progression of the pandemic and the future state of the economy are creating two very different scenarios for consumer debt.

One is encouraging. Bob Leger, chief financial officer at Infinity Federal Credit Union in Westbrook, is seeing customers who are able put more money into savings and pay down credit card debt. Contrary to typical behavior, some homeowners are taking advantage of low interest rates to refinance 30-year mortgage loans into shorter terms. They’ll have higher monthly expenses but will pay down their mortgages more quickly.

“It seems that consumers are reacting to this high degree of uncertainly by changing their savings habits and their relationship to debt,” Leger said.

But the picture is darker for Mainers with accumulating bills. When the grace periods end, when the subsidies run out, experts expect a rush of collection attempts from creditors.

“We certainly are bracing for a period that will start in a couple of months and extend at least a year beyond that,” said Will Lund, superintendent at the Maine Bureau of Consumer Credit Protection.

Lund can gauge creditor activity by the number of applications from debt collectors and repossession companies that must register to do business in Maine. It’s steady now, but he expects that to change.

Lund has some suggestions for Mainers in debt:

• Check your credit history. The nation’s three credit reporting agencies are offering free weekly online reports through next April.

• Communicate with lenders and creditors. Confirm any agreement with a dated copy in writing, as a way to document what the parties agreed on, in case there’s a dispute in the future.

• Be careful about getting sidetracked online by for-profit companies selling credit monitoring or other products.

“The next six months to a year will be a challenging time for consumers,” Lund said. “There’s no doubt about that.”

Send questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.