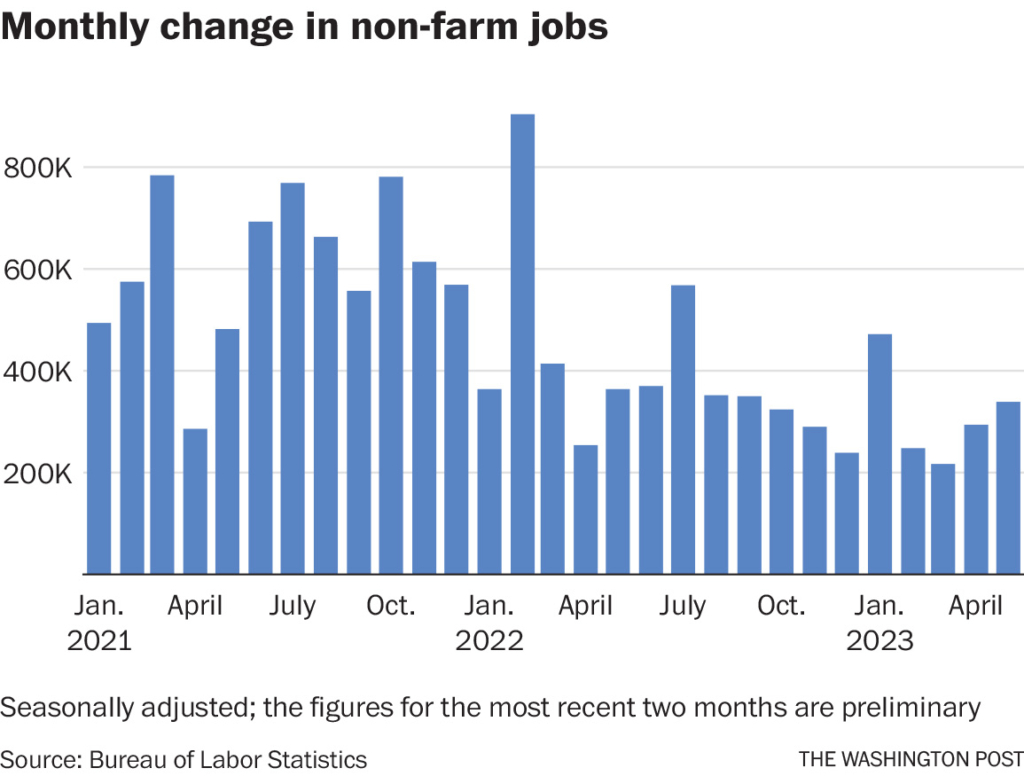

Employers added 339,000 jobs in May, in the latest sign that a booming labor market is keeping the country from slipping into a recession.

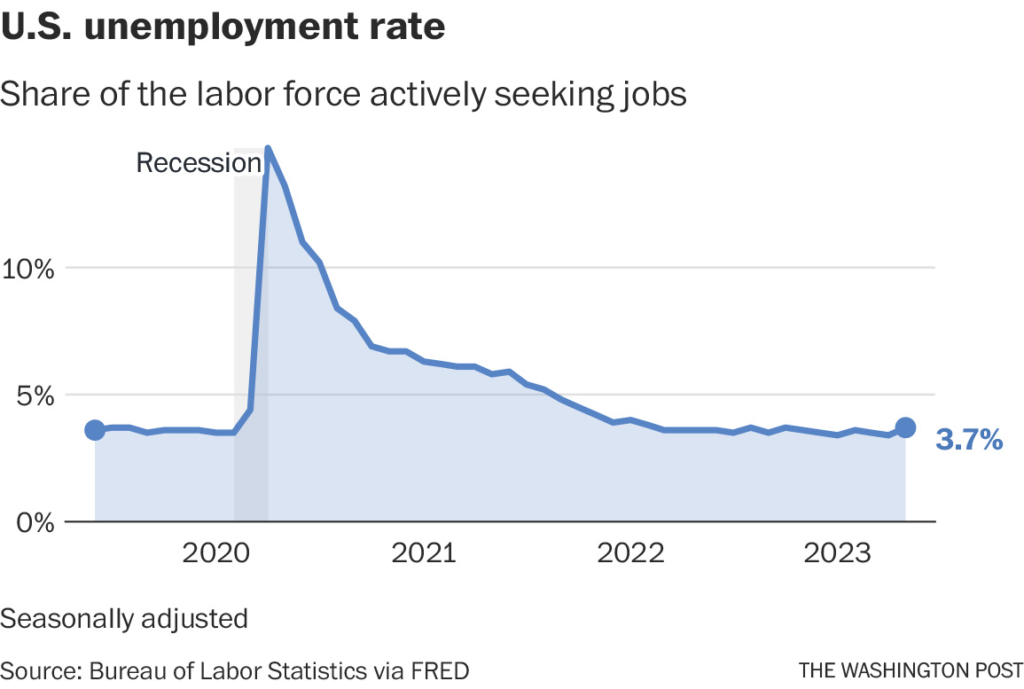

The unemployment rate rose to 3.7% last month, up from 3.4%, the Bureau of Labor Statistics reported Friday.

The May jobs report reveals the 29th straight month of strong job growth that has come to define the pandemic recovery economy. Economists had predicted 180,000 jobs created.

For months, employers have churned out jobs at a rate that has baffled economists. And the labor market has propelled the economy through a barrage of forces that would normally weigh on jobs creation – steep interest rate hikes, bank failures, and several rounds of layoffs in tech, hitting 200,000 workers this year, according to the tech layoff tracker Layoffs.

“We are not currently in a recession, but we are likely to see one towards the end of this calendar year,” said Rand Ghayad, head of economics and global labor markets at LinkedIn. “The resilience and robustness of the U.S. labor market mean the economy can absorb more Fed rate hikes than we previously thought.”

Many economists are predicting a recession later this year, especially if the Federal Reserve keeps hiking interest rates to curb inflation.

“We’re likely to experience some kind of contraction in at least the second half of 2023, but job growth has pushed back [our expectations],” said Matt Colyar, an economist at Moody’s Analytics.

There are many other signs that the labor market remains healthy. New applications for unemployment benefits, often an early predictor of recessions, remain low. And job openings unexpectedly soared by half a million in April, according to new data from the Bureau of Labor Statistics released Wednesday.

Overall wage growth, although not keeping up with inflation, is rising faster than it has in years for earners on the lowest end of the wage scale. Meanwhile, the Black unemployment rate fell to the lowest rate on record in April.

Beyond the labor market, there are other reasons for optimism. Consumer spending, which drives the U.S. economy, increased in April after two months of a slowdown, according to the Commerce Department. Congress passed a deal to avoid a catastrophic U.S. government default that might have triggered millions of job losses. And the financial markets have rebounded in recent months.

Elise Gould, a labor economist at the Economic Policy Institute, a left-leaning think tank, said that the covid stimulus packages enacted by the government have helped create consumer demand that has carried the labor market through a storm of economic uncertainty.

Still, there are signs that the economy is cooling down. The U.S. economy faltered in the first months of 2023, growing at a lackluster annual rate of 1.1%. Manufacturing output has weakened, and credit lending – which gives employers more ability to expand and hire – has tightened up.

There has also been some evidence of cooling in the labor market. Unemployment insurance claims, though historically low, have risen by more than 25% since their low point in 2022.

Jobs openings have begun to fall in the service sector, including in leisure and hospitality, and government, areas that were booming earlier this year. The rate of workers who quit their jobs fell in April, almost returning to its pre-pandemic levels, suggesting workers are less confident in their ability to switch jobs than they were last year.

Layoffs, although higher than a year ago, fell in April even as mass job cuts swept through tech companies, such as Meta and Lyft, making headlines.

“The story is that the economy’s been weak and it appears it will get weaker,” said Joseph LaVorgna, chief economist at SMBC Nikko Securities America. “But there isn’t any obvious sign that the labor market is about ready to go off a cliff.”

Some industries are faring worse than others. For months, the transportation and warehousing industry has weathered slow job growth, with little change in employment for the past two months. Coming out of the pandemic, consumers shifted their spending away from goods, such as online shopping, and infused their earnings into services, such as travel and dining out. Meanwhile, a supply chain crisis during the pandemic that created a backlog of demand has largely been resolved.

Amazon has canceled, closed, or delayed dozens of new facilities, and laid off thousands of corporate workers since last year. (Amazon founder Jeff Bezos owns The Washington Post.) Walmart, meanwhile, laid off more than 2,000 warehouse workers in April. Other logistics companies – large and small – have slowed hiring, and shrank their workforce by not filling openings as workers quit.

“Consumer demand for products has gone down,” said Patrick Penfield, a professor of supply chain practice at Syracuse University. “We’re seeing warehouses and trucking companies laying off people. Their goal is to try to survive a recession.”

Despite relatively concentrated pockets of cooling, American consumers and workers are increasingly pessimistic about the future of the economy. Consumer sentiment sank to a six-month low last month, according to a University of Michigan consumer survey. Job seekers have become more concerned about labor market conditions and their finances in the first quarter of 2023 than they were last year, according to ZipRecruiter’s job seeker confidence index.

Copy the Story LinkSend questions/comments to the editors.

Success. Please wait for the page to reload. If the page does not reload within 5 seconds, please refresh the page.

Enter your email and password to access comments.

Hi, to comment on stories you must . This profile is in addition to your subscription and website login.

Already have a commenting profile? .

Invalid username/password.

Please check your email to confirm and complete your registration.

Only subscribers are eligible to post comments. Please subscribe or login first for digital access. Here’s why.

Use the form below to reset your password. When you've submitted your account email, we will send an email with a reset code.